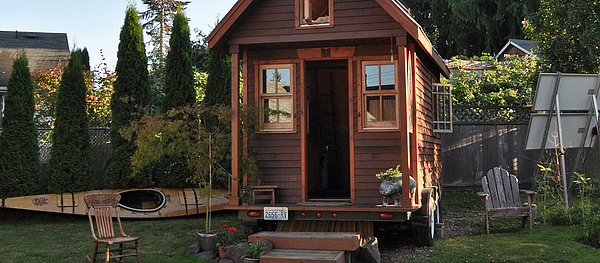

Dee Williams from Portland Alternative Dwellings is excited to announce that she has found an insurance company willing to insure tiny houses on wheels. Dee tells it so much better so I will let her take over from here…

Plenty of other folks have also been stewing over how to best protect tiny house owners from catastrophic loss. I’ve got good news for you today! I found someone willing to give real, substantial insurance to tiny houses that treats them like home worth protecting.

Now, Darrell Grenz of Portland, Oregon has networked with Lloyd’s of London to develop a policy that will cover the market value of a tiny house, plus your possession,s in the event of a fire or more if you live deep in the country with remote access by the fire department. That amount is due up front; there are no monthly payments because there’s no financing for the package. But that seems reasonable given the peace of mind that comes with knowing you’re covered — really covered.

At this time the policy is only available to tiny housers in California, Nevada, Oregon, Utah, Colorado, Arizona and Washington. Other states may be adopted later.

To get the full scoop and contact information visit the PAD website link here: http://padtinyhouses.com/real-insurance-for-tiny-houses-on-wheels/

It’s time to enter the mainstream!

Before anyone gets all excited about a Lloyd’s Policy, there needs to be a close review of the an actual policy and the fine print and a complete and total list of exclusions. Lloyds is not an actual insurance company in the traditional sense, but brings investors together to provide coverage for a contract.

Llyods will insure ANYTHING if the premium can be paid upfront. This includes loaded oil tankers moving thru a war zone, so people need to understand what Llyods is and exactly how and what they do.

Any insurance agent can submit a proposal for insurance to Llyods.

This news is good for those interested and wanting to insure, but personal research and the exact policy disclosures are needed for review before a Llyods policy is considered standard coverage for a tiny house.

Just my opinion, but small home/tiny house insurance is just another financial market expense that can be dropped from the owners budget

if the owner establishes some fallback emergency funds AND has some skills to rebuild or repair.

Insurance companies are nothing more than investment companies at their core.

Anyone financing small builds does not have that option.

A lot more details are needed on this.

‘It’s time to enter the mainstream!’

No Thanks! Trying to leave it in the dust, where it belongs. Don’t feed the insurance scam artists.

Just self-insure and save the money. IOW, put that payment into the bank each month and when you have the amount your house is worth, you can cover it yourself if something happens. IF nothing ever happens, you still have your money.

Sure, there’s a small risk that something will happen in the meantime, and insurance companies like reminding you of that, but the odds are pretty small.

Yes, I agree with the concept of self insurance for this sort of thing. But it’s still not an appropriate solution for everyone. Some people just simply won’t have the funds won’t ever… or for a very long time…. to rebuild at all is the whole thing burns or rolls / demolished etc…

Insurance is not always a scam. I functions quite literally are as a form of ‘community bank’ everyone puts in a little for form a pool of cash. So when a member of the pool suffers a big loss… the community takes care of it. In essence, insurance is a form of communism.

Yay!! Thanks, Dee & Darrell! Having insurance might help get changes in local permitting as well.

It’s time to go mainstream! The times they are a’changin’!

Curious. Can’t a person get ‘renter’s’ (or ‘personal property’?) insurance to cover their possessions (furniture, keepsakes, clothing, etc), regardless of whether they own, rent, lodge with others or travel? Because if so, I’d forgo the home insurance, too, putting an amount relative to an insurance premium away every month, as others suggested, hoping to have squirreled enough away in a few years to basically be there ‘in case’ my home would have to be replaced/rebuilt, but property insurance would always be there to guard and replace all personal effects, etc. Unless there is no policy for ‘property/personal possessions’ when living in a tiny house…?

Don’t even bother considering insurance. Where I live the tallest buildings are owned by insurance companies, the most notorious white collar fraud was done by insurance companies. Save your cash.

As for ‘mainstream’, even paying an insurance broker to find the most comprehensive insurance at the best price you will be ripped off. It happened to me.

As another alternative, we have insured our tiny homes with a local Allstate Insurance agent. It was full coverage RV insurance, very reasonable. You just have to have your car with them as well. Assume this is not an issue other places. Any insurance company that insures RVs should not be a problem. Bill Kastrinos Tortoise Shell Home

I’ve always read that a big aspect of living tiny is to have options, because no one option is ever going to work for all people. So if you don’t want insurance for your tiny house, don’t get it. Some people, though, do want it. It’s always good to have options.

http://tinyhouseblog.com/announcement/tiny-house-wheels-insurance/

Sorry, posted on the wrong article. Please disregard.